+91 9983 203 203

Latest articles on Life Insurance, Non-life Insurance, Mutual Funds, Bonds, Small Saving Schemes and Personal Finance to help you make well-informed money decisions.

|

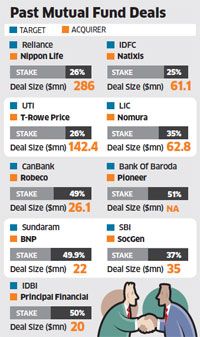

L&T Finance has agreed to buy Fidelity Worldwide Investment’s Indian mutual fund business, becoming the 10th-biggest equity fund house in a highly fragmented and competitive market marked by wafer-thin profitability. The financial services arm of construction major Larsen & Toubro pipped rivals, including HDFC Asset Management and Pramerica, to purchase FIL. The deal will immediately boost L&T’s assets to Rs 13,500 crore, making it the 13thbiggest fund and the 10th-largest on the basis of equity. "A large part of the L&T Finance business is lending. This is part of the move to increase fee-based income which is a steady business over mid-to-long term," YM Deosthalee, chairman & managing director of L&T Finance Holdings, told a press conference. Shares of L&T Finance rose 4.6% to close at Rs 49.80 on Tuesday after a late spurt. "It will be a turning point for L&T Mutual Fund and sad for the mutual fund industry, because a good fund house has decided to walk out of the country," said Dhirendra Kumar, managing director of fund tracker Value Research. Experts say the deal will confer size on L&T. |

|

However, the deal does not include the equity fund management team led by Alexander Treves, the chief investment officer of Fidelity Mutual Fund. "The equity fund management team will be with us till the integration process is complete," said Deosthalee. He said Fidelity’s India Chief Executive Officer Ashu Suyash will be a key part of the integration process. As per the agreement, L&T will absorb most of the employees of Fidelity Mutual Fund. "Fidelity employees need not worry about this deal. L&T Finance is an equally strong brand. And historically, Indian funds have done much better than foreign fund houses," Deosthalee pointed out. The deal comes at an opportune time for Fidelity, which is facing a regulatory deadline to shift its trading desk to India by September. The mutual fund industry has lurched from crisis to crisis since the global financial meltdown of 2008. The ban on entry load, the upfront fee that mutual funds charged investors to pay distributors, in August 2009 has compounded their woes as distributors now have lesser incentive to sell schemes. The key challenge for L&T will be to retain investors in Fidelity funds, many of whom had invested in the ’Fidelity’ brand. The deal will not make any sense to L&T if it fails to retain these investors, industry sources said. This is more so because apart from assets under management, which can be fickle most of the time, L&T Mutual Fund has not been able to buy out the experienced equity fund management team of Fidelity. But L&T could take heart from the performance of Templeton and HDFC asset management houses after their takeover of Zurich and Kothari Pioneer in the early years of the past decade. The buyouts happened just before the equity boom of 2004-08, helping both fund houses build a sizeable advantage over rivals. "We’ll be able to retain investors... We’re an equally good brand. We have good fund management capabilities to satisfy investors. |

Follow us on our social media channels:

Copyright © 2026 Design and developed by Fintso. All Rights Reserved

Industry News

Industry News