+91 9983 203 203

Latest articles on Life Insurance, Non-life Insurance, Mutual Funds, Bonds, Small Saving Schemes and Personal Finance to help you make well-informed money decisions.

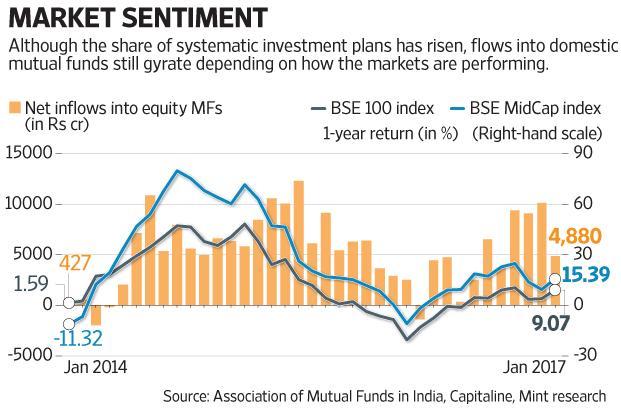

Indian equity mutual funds (MFs) have received net inflows of a little over Rs2 trillion since May 2014. Monthly inflows stood at around Rs6,100 crore during this period. In recent months, inflows from systematic investment plans (SIPs) alone have amounted to around Rs4,000 crore per month.

Despite heavy selling by foreign institutional investors since the demonetisation announcement, Indian markets have done well, largely because of large purchases by domestic institutions.

As a result, some investors are enthused about domestic flows sustaining Indian equities going ahead as well. Analysts at UBS Securities India Pvt. Ltd say in a note to clients, “In our discussions with investors, they saw inflows into local Indian equity mutual funds as a reason to be bullish, especially as these have offset selling by foreigners in late 2016, and there are hopes that this is a structural trend.”

Investors are all the more gung-ho since flows through SIPs are estimated to be sticky. Analysts at Deutsche Equities India Pvt. Ltd said in a recent note to clients, “We estimate that SIPs would have accounted for a healthy ~43% of total equity inflows over the past six months. If this trend sustains into the future, as per industry experts, SIP-based monthly inflows have the potential to average ~US$1bn (~Rs6,800 crore) over the next few years.”

But note in the chart alongside how inflows into equity MFs are still closely related to the market’s short-term returns. When returns of large-cap and mid-cap indices went into negative territory in early 2016, flows into equity funds tapered. Since the period where one-year returns were negative was short-lived, the drop in outflows, too, was restricted to a short period.

As UBS’s analysts say, “Investors should not look at a decrease in local flows as a lead indicator for Indian markets—flows will follow returns rather than the other way round.” They add that apart from market returns, the relationship of flows with interest rate movements and returns on alternative asset classes suggests that flows to equity funds should find support in the near term.

As such, even if, as many expect, Indian companies disappoint in the March quarter, their stocks may find support from domestic institutions. But as pointed out earlier, it may be naive to expect this to continue forever. UBS points out that despite all the arguments that support the theory that the increase in domestic flows is structural, the fact remains that financial savings as a share of household savings are now lower compared to levels in fiscal years 2006-2008. “In FY06-08, many market watchers also argued that local flows were ‘structural’,” they add in their note. We all know how that ended.

Industry News

Industry News